Summary

Highlights

The US technology sector is leading earnings growth for Q4 but markets are no longer giving a free pass to these businesses.

Secondly, earnings growth is broadening and is no longer concentrated in a small number of technology firms.

Although the reporting season was positive, market concerns persist about AI-distruption and the monetization of AI-investment.

In this edition

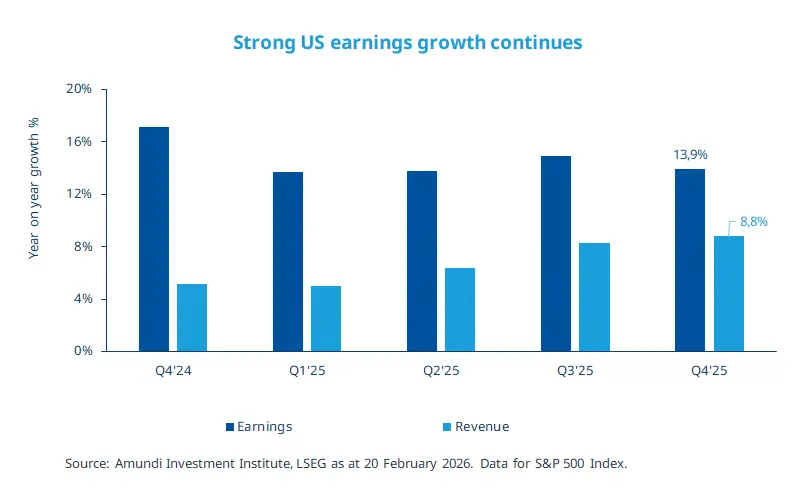

US equities saw another strong reporting season for the three months (Q4) ended 31 December 2025, with blended (actual earnings of companies that have reported results plus estimated earnings of those yet to report) earnings growth of about 14% year-on-year, as on 20 February 2026. While this earnings growth is slightly below what we saw in Q3, it is much higher than the estimate at the start of the reporting season (about 9%). Information technology is once again leading but there are continued signs of earnings broadening with strong results from the industrials, financials and communication services. In Europe, the reporting season has been relatively muted, with no growth at the index level. But more companies are yet to report earnings in Europe. Financials once again have had a strong quarter with meaningful upgrades, whereas the cyclical consumer sector continues to be a drag.

Key dates

EZ PMI, Germany Retail Sales, Turkey GDP, US ISM Manufacturing |

China PMI, EZ PMI Services and Composite, US ISM Services |

EZ GPD, US Retail Sales and Non Farm Payrolls, South Korea CPI, Brazil Industrial Production |

Read more