Summary

Highlights

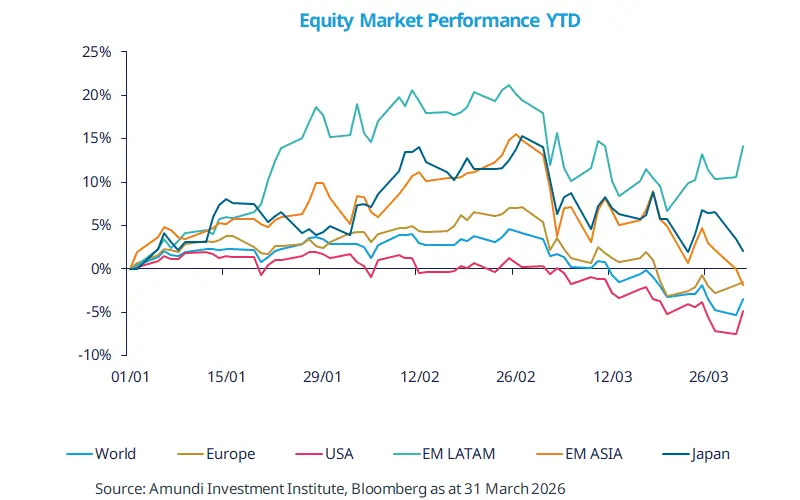

The Iran crisis has triggered a repricing in equities, with most regions coming under stress - US more so than others, year to date.

Long-term, the rotation towards Europe, Japan and EM may play out in different phases and could be affected by how long energy prices remain elevated.

In our view, adding multiple layers of diversification*, seeking returns across the asset class spectrum and maintaining safeguards in place may support a more resilient portfolio.

In this edition

The year-to-date has been characterised by a series of geopolitical events. While markets largely shrugged off the US military action in Venezuela, the war in the Middle East triggered a sharp rise in energy prices, with knock-on effects across global markets. Consequently, equities declined worldwide, and bond yields rose. Markets are pricing in aggressive central bank actions, as they are overly concerned about inflation, whereas growth worries are on the backburner at the moment. We agree only partially with the markets but believe growth may be affected if prices stay high for a long period.

The impact of the crisis on equities was not uniform. Energy-importing countries and those that had performed strongly before the start of the war were more affected. Despite this heightened uncertainty, year-to-date performance in selected emerging markets — particularly Latin America — and Europe has been better than in the US. Looking ahead, this crisis reinforces our view that diversification* across regions such as emerging markets, Japan and Europe is key to long-term resilience.

* Diversification does not guarantee a profit or protect against a loss

Key dates

USA ISM service, EA PMI. |

EA Retail sales, US Fed Meeting Minutes. |

US PCE Index, Jobless Claims, GDP 4T. |

Read more